There are two tax systems operating on your life simultaneously. One is visible, centralized, debated in parliaments, reported in budgets. The other has no face, no ballot, and no line on your tax return — yet for most people in privatized economies, it costs more of their working life than the first one ever will.

The Invisible Hand That Picks Your Pocket

In 1776, Adam Smith wrote of an "invisible hand" guiding self-interested market actors toward outcomes that benefit society as a whole. It was a modest, qualified observation — used only three times across his entire body of work. Two centuries later, it had been transformed into something else entirely: the theological cornerstone of a global economic ideology that subordinated democratic governance to the logic of capital markets.

This transformation — from a tentative metaphor to an unquestionable natural law — is the subject of The Invisible Doctrine by journalist George Monbiot and filmmaker Peter Hutchison. Neoliberalism, they argue, is simultaneously all-encompassing and seldom, if ever, explicitly named. The ultra-rich were cast as heroic "independents" staking out new territory beyond the reaches of nefarious governments — and from this foundation, the doctrine that markets always allocate better than democratic institutions was systematically installed into university departments, political parties, media organisations, and the operating assumptions of governments worldwide.

George Monbiot & Peter Hutchison · Penguin Books, 2024 · Also available as a documentary film (2025). A short, sharp, forensic account of how a fringe philosophy in the 1930s became the operating system of global economic policy — and what it has cost us in democracy, ecology, and the fabric of public life.

The consequences are visible everywhere: privatisation leads to a decline in both access to, and the quality of, public services. Healthcare under privatisation becomes a gamble. Education becomes a commodity, accessible only to those who can pay. Housing is transformed into a speculative asset class, pushing millions into precarity.

The Private Tax framework challenges the invisible hand doctrine: not a values argument, but a measurement one. If markets allocate efficiently, that efficiency should be evidenced in the universal currency of human time. When we count — for any given service — how many work hours of your life does each delivery model cost, the invisible hand becomes very visible indeed. And it's not allocating efficiently. It is extracting.

The same invisible hand that supposedly allocates efficiently is the hand in your pocket. The Private Tax framework simply counts what it takes — in hours of your finite life.

Public taxes are centralized and visible. You see them: on your pay stub, debated in the legislature, reported in the news. There is a public face to the transaction — a mechanism you can challenge, vote on, or contest. Private taxes are different in every respect: distributed, opaque, shapeshifting behind narrative masks — market efficiency, consumer choice, shareholder value, competitive pricing. Never named as a tax. Now, we can name it and measure it.

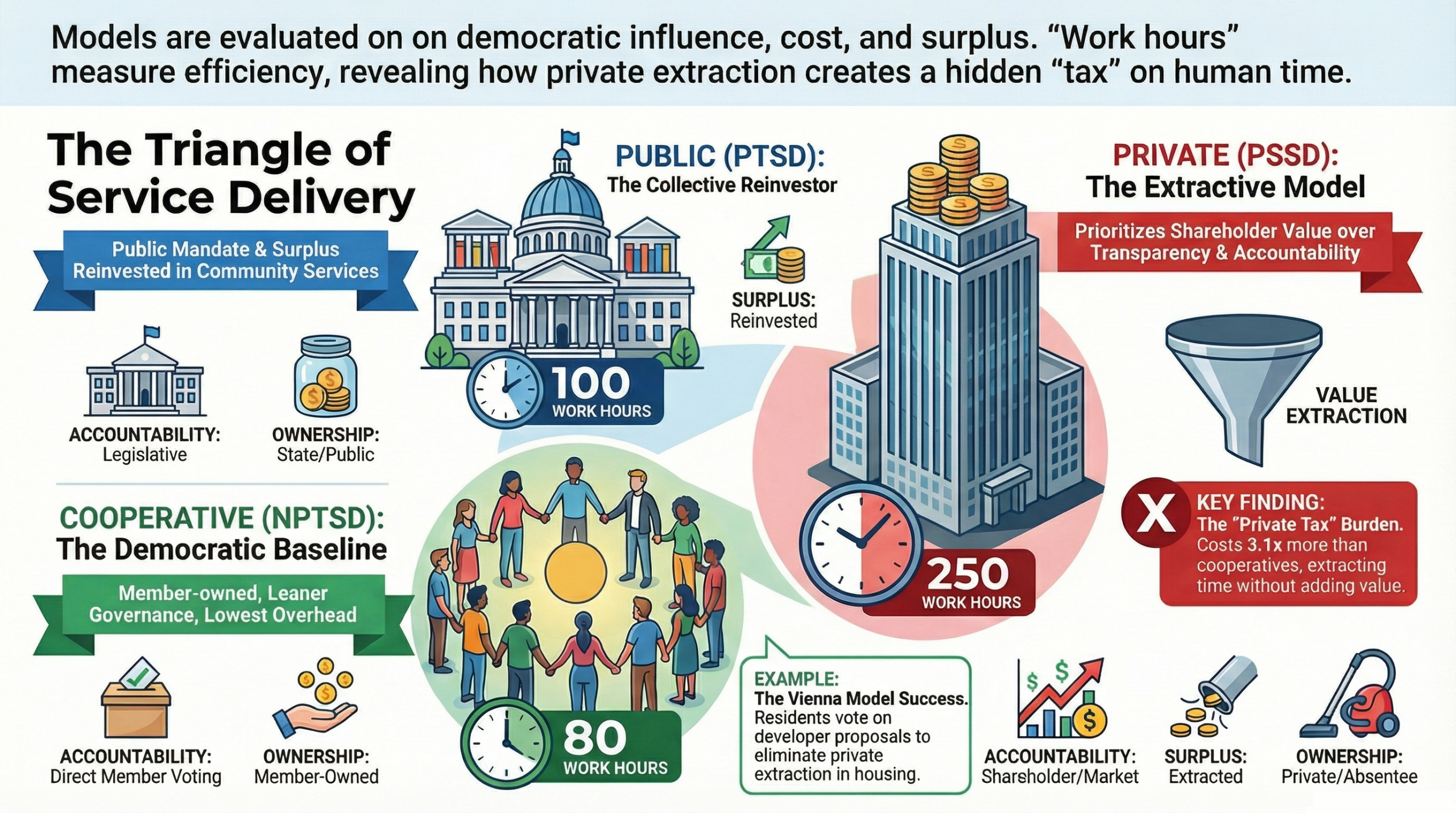

The Triangle of Service Delivery

Any good or service provided to a population can be delivered through one of three structural models. Each has a fundamentally different relationship to democratic accountability, cost overhead, and the distribution of surplus. To measure their relative costs, we first define them precisely.

Public Tax System Delivery

The population has, ideally, democratic influence over the good faith political actors operating the system. Overhead is constrained by public mandate. Surplus is reinvested into services benefiting the population, rather than extracted through privatization. Funded through tax revenue backed by collective income and low-cost treasury financing.

Non-Profit / Cooperative Delivery

A cooperative or non-profit entity delivers the equivalent service. Every member votes on budget and service fees. Transparent, democratically operated, and directly accountable to its membership. Structurally equivalent to democratic public delivery in terms of accountability, with operational efficiency advantages at neighbourhood-to-city scale — including lower overhead and leaner governance structures.

Private Sector Service Delivery

When a for-profit private corporation delivers the service, surplus is extracted to shareholders rather than reinvested or returned to users. No democratic accountability. Narrative control is exerted through the common tropes of "choice," "competition," and "efficiency" — these narratives replace transparency about cost structure.

Model B — Non-Profit / Cooperative Delivery (NPTSD) — is treated as the democratic efficiency baseline: structurally equivalent to public government in terms of member accountability, but with the additional advantage of direct member ownership. The cooperative model is well-established, neutral in governance, and requires no affiliation with any particular platform or currency system to understand.

The distance between Model B (NPTSD) and Model C — Private Sector Service Delivery (PSSD) — measured in work-hours of human life, is what we are calling the Private Tax Burden. The invisible hand's fee for its services. Counted in time.

Work Hours as the Universal Currency

The standard measures of economic comparison — price, GDP, cost-of-living indices — are denominated in money, which is subject to inflation, manipulation, and context-dependence. A dollar in 1980 is not a dollar in 2026. A dollar in Vancouver is not a dollar in a rural town two hours away.

But an hour of your life is an hour of your life. It is the one currency perfectly equalized across every person and every era. We all receive the same 24 hours per day. The question is: how many of those hours must you surrender as work in order to receive a given service?

Time is the only currency that cannot be inflated, cannot be printed, and cannot be redistributed. It is the truest measure of burden — and the most direct measure of what any economic system actually costs you.

This is the foundation of the LTE Index (Life Time Efficiency) — the broader framework within which Private Tax analysis sits. The LTE Index measures how much of a person's working lifetime is consumed by the cost of living, rather than available for everything else that makes a life worth living: relationships, creativity, rest, civic participation. Its companion measure, the Time Extraction Index (TEI), isolates the parasitic portion of that consumption — the share flowing not into service delivery but into financial extraction with no corresponding service value.

Private Tax analysis applies this framework at the service level. For any given service, it asks: how many more hours of your finite life does the for-profit delivery model cost you, compared to public or cooperative alternatives? That surplus — in hours, days, and months of your working life — is the Private Tax. It is being collected whether you see it or not. The invisible hand is not invisible because it doesn't exist. It is invisible because we have been given no instrument to measure it. The Time Differential Ratio is that instrument.

The Time Differential Ratio

To move from concept to measurement, we define two key differentials and a ratio that relates them. In all equations, T represents work time measured in hours — the hours of your life required to pay for a given service under each delivery model. D represents the delivery differential — the time-cost difference between any two models, whether that difference is a premium (more hours) or an advantage (fewer hours).

Core Equations

| Term | Equation | Plain-Language Meaning |

|---|---|---|

| TD¹ | PSSD − NPTSD | The time premium of Model C – Private (PSSD) over Model B – Cooperative (NPTSD). The raw hours of your life extracted above and beyond the cooperative cost of the same service. |

| TD² | PTSD − NPTSD | The cooperative efficiency advantage — how many hours per year Model B – Cooperative (NPTSD) saves relative to Model A – Public (PTSD). Reflects the absence of bureaucratic overhead and leaner governance in the cooperative model. A positive number means the cooperative is more efficient than public delivery. |

| TDR | TD¹ ÷ TD² | Time Differential Ratio — how many times larger the private extraction premium (TD¹) is than the cooperative efficiency advantage (TD²). A high TDR is the structural fingerprint of extraction rather than genuine operational cost difference. |

| PTB | (PSSD ÷ PTSD) − 1 | Private Tax Burden as a percentage premium above the public baseline (Model A – PTSD). The share of every hour you work for this service that delivers no additional value — it flows directly into shareholder extraction. |

The Efficiency Comparison Ratio

We can compare any two models directly as a multiplier — asking simply: how many times more of your life does Model C – Private (PSSD) cost compared to Model A – Public (PTSD) or Model B – Cooperative (NPTSD)? This Efficiency Comparison Ratio (ECR) makes the Private Tax Burden immediately legible without requiring calculation.

An ECR of 2.5 between Model C – Private (PSSD) and Model A – Public (PTSD) means: to receive the same service under a for-profit model, you must work 2.5 times longer than under public delivery. The extra 1.5× — meaning 150 additional hours for every 100 hours of public-equivalent cost — represents pure extraction. Value produced by your labour flows to shareholders rather than back into the service you received.

This is the Private Tax. It is not collected by a government. It is not debated in parliament. It does not appear on any ballot. But it is collected, reliably and systematically, every time you pay for a privatized service. The invisible hand is not allocating efficiently. It is allocating — to itself.

Three Models, One Service: The Numbers

To make this concrete, consider a single representative service — home insurance, internet provision, or pharmaceutical supply — measured across all three delivery models in annual work hours required to pay for it.

| Delivery Model | Abbrev. | Annual Work Hours Required |

|---|---|---|

| Model A – Public Tax System Delivery | PTSD | |

| Model B – Non-Profit / Cooperative Delivery | NPTSD | |

| Model C – Private Sector Service Delivery | PSSD |

Efficiency Comparison Ratios

Expressing each model as a multiple of the public delivery baseline (Model A – PTSD = 100 hrs), with Model B – Cooperative (NPTSD) at 80 hrs — 20% more efficient than public delivery:

Time Differential Ratio (TDR) Calculation

| Term | Calculation | What It Means |

|---|---|---|

| TD¹ | 250 − 80 = 170 hrs | The private extraction premium above Model B – Cooperative (NPTSD). 170 hours of annual work-time that deliver no additional service value — pure shareholder extraction. |

| TD² | 100 − 80 = 20 hrs | The cooperative efficiency advantage over Model A – Public (PTSD). Model B saves 20 hours per year through lower overhead and leaner operations. A positive number confirming the cooperative is the most efficient baseline. |

| TDR | 170 ÷ 20 = 8.5× | The private extraction premium is 8.5 times larger than the cooperative efficiency advantage. This is the structural fingerprint of systematic extraction — a difference of this magnitude cannot be explained by operational costs. |

The TDR of 8.5 is the key diagnostic number. It tells us that the step from Model A – Public (PTSD) to Model B – Cooperative (NPTSD) is not a premium at all — it is a 20-hour saving, the dividend of member ownership, lean governance, and lower operational overhead. But the step from Model B – Cooperative to Model C – Private (PSSD) is 8.5 times that magnitude, and moves entirely in the wrong direction. That asymmetry cannot be explained by operational costs. It is the structural fingerprint of the invisible hand at work — allocating, systematically, to itself.

Private Tax as a Dimension of the LTE Index and TEI

This analysis does not stand alone. It extends the Block Share framework for measuring the true cost of economic systems on human lives — specifically the LTE Index (Life Time Efficiency) and the Time Extraction Index (TEI).

Connection to the LTE Index

The LTE Index frames economic burden as a percentage of working lifetime consumed by the cost of maintaining a given standard of living. A city with an LTE Index of 99% means that 99% of working hours are consumed by basic costs — leaving almost nothing for the rest of life. Vancouver currently sits near that ceiling.

Private Tax analysis extends this logic from the aggregate to the service level. Rather than asking "what share of your total lifetime is consumed?" it asks, service by service: "what share of your lifetime cost for this service is pure extraction — hours flowing to shareholders rather than back into service delivery?" The Private Tax Burden (PTB) percentage becomes a service-level LTE Index component. Applied systematically across healthcare, insurance, housing, utilities, telecommunications, and financial services, it produces a comprehensive map of extraction embedded in the cost of living — invisible in aggregate statistics, clearly legible in life-hours.

Connection to the TEI

The Time Extraction Index (TEI) separates the parasitic extraction component of economic systems from genuine value creation. In housing analysis, we used the TEI to distinguish mortgage principal — real shelter value — from mortgage interest, which is financial extraction. The same logic applies here: the private delivery premium (TD¹) is the TEI applied to services. It is the portion of your payment that delivers nothing additional; it simply routes value from your labour to a shareholder. The TDR gives the TEI a service-level expression: a TDR of 8.5 tells us the extraction component is 8.5 times the size of the cooperative efficiency advantage over public delivery — the ratio of extraction to genuine operational difference.

The Private Tax Index (PTI)

Over time, this framework enables construction of a Private Tax Index (PTI) — a sector-by-sector account of the extraction premium embedded in privatized service delivery, expressed in lifetime hours and as a percentage of the LTE Index. This allows direct empirical comparison across cities and policy regimes: not "does privatization cost more?" (it does) but "exactly how many months of your working life does privatization cost you, and across which sectors?" It transforms a political argument into an accounting one. And accounting is harder to argue with than ideology.

The Hand, the State, and the Cooperative Alternative

Every time a government privatizes a public service — or fails to consider returning a privatized one to public or cooperative management — an implicit transfer is made. In our illustrative example here, that transfer represents a premium of approximately 150% in time-cost per service, per household, per year — redirected from the lifetime accounts of every user of that service to the income accounts of shareholders. Applied across multiple privatized services, that cumulative percentage becomes months of working life annually.

But the more important policy insight from this analysis is not simply the case against privatization. It is the case for cooperative and public ownership — and the measured cost of the neoliberal doctrine that has systematically displaced them over the past fifty years.

It would be an oversimplification to position government delivery as uniformly superior without acknowledging its own inefficiencies. Policy is frequently shaped not by public debate or democratic accountability but by the calculus of corporate profit. Governments are subject to private-sector lobbying, short electoral cycles that discourage long-term infrastructure investment, and political incentives that favour announcements over outcomes.

The cooperative model inherits the accountability virtues of democratic government — member votes on budgets and service specifications — while being structurally insulated from the political economy vulnerabilities that compromise government delivery. It is not a theoretical ideal; it is a proven institutional form with a long operational track record across housing, insurance, utilities, banking, and food systems worldwide.

Cooperative Ownership as a Structural Private Tax Elimination

The cooperative model has a structural property that neither government nor private corporations share: the population served are simultaneously owners, users, and beneficiaries of the infrastructure they collectively hold. This creates an institutional bias toward long-term efficiency and resilience — the opposite of shareholder extraction logic.

When housing, utilities, broadband, and local services are held as cooperative assets, the private sector loses its primary entry point: capital scarcity and the information asymmetry between providers and users. The Private Tax is not just reduced; it is structurally displaced. The invisible hand's fee drops toward zero not because of regulation, but because the mechanism of extraction — absentee ownership, information asymmetry, artificial scarcity — has been removed from the equation.

Global Precedents: Public Land, High Ownership, Low Time-Cost

The proposition that public or cooperative land and infrastructure ownership produces efficient, high-quality services at low time-cost is not theoretical. Several countries demonstrate it at scale — not through coercion, but by offering a demonstrably more efficient model that populations choose because it works and because the Private Tax on housing approaches zero when land is de-commodified.

| Country / City | Housing Rate | Land Model | Key Features |

|---|---|---|---|

| China | ~95% | State Land Lease | All land publicly owned; residents hold long-term use rights on structures. Housing is treated as infrastructure rather than a speculative asset class. Private extraction of land value is structurally prevented rather than regulated. |

| Singapore | 80–90% | Public Land + HDB | Housing Development Board builds and manages approximately 80% of housing stock on state-owned land. Prices are set relative to income, not market speculation. The result is some of the highest home ownership rates in the world at a fraction of the time-cost found in fully privatized markets. |

| Vienna, Austria | 60% social | Municipal + Cooperative | Residents specify what gets built. Developers and builders submit competing proposals; residents vote on which to approve and fund. The population designs its own housing infrastructure — the cooperative principle applied at city scale, with the private sector playing a delivery role under democratic direction rather than market control. |

What these models share is not state coercion but structural efficiency: when land and key infrastructure are removed from the speculative market, the Private Tax on the most significant single component of the cost of living approaches zero. The LTE Index improves dramatically — not because wages rise, but because extraction is removed from the equation. The invisible hand is shown the door.

Vienna's model is particularly instructive: it is not government dictating what gets built — it is government providing the framework within which residents vote for what they want built and who builds it. The population retains agency. The developer retains a role. But the extraction premium disappears, because the land value accretes to the community rather than to private capital. The invisible hand allocates. Just not to itself.

The Block Share Application

The Block Share / Community Credyts ecosystem is, in one sense, an applied response to Private Tax burden at neighbourhood scale. By building cooperative resource-sharing infrastructure — with democratic governance, open accounts, and surplus returned to members — it operates structurally as Model B – Non-Profit / Cooperative Delivery (NPTSD) rather than Model C – Private Sector Service Delivery (PSSD). The LTE Index improvement from participating in a Block Share neighbourhood is, in measurable part, a Private Tax reduction: hours of your life reclaimed from extraction and returned to living.

Community Credyts — denominated in time rather than dollars, issued against real labour and assets — make the time-cost accounting explicit in every transaction. When you earn and spend Credyts, you are operating in the framework this article describes. The currency itself is a Private Tax measurement instrument — and a reduction instrument simultaneously.

The next step is making the measurement systematic: applying the TDR and PTI to the services most commonly accessed by cooperative and Block Share communities — insurance, childcare, eldercare, telecommunications, energy, housing — and publishing those numbers as community knowledge. Not advocacy. Accounting. The invisible hand, finally, in plain sight.

Abbreviations & Terms

Standard Abbreviations — Private Tax / LTE Index Framework

- PTSD Model A – Public Tax System Delivery

- NPTSD Model B – Non-Profit / Cooperative Delivery

- PSSD Model C – Private Sector Service Delivery

- TD¹ Time Differential 1 — private extraction premium (PSSD − NPTSD)

- TD² Time Differential 2 — cooperative efficiency advantage (PTSD − NPTSD)

- TDR Time Differential Ratio (TD¹ ÷ TD²)

- PTB Private Tax Burden (PSSD ÷ PTSD − 1, expressed as %)

- PTI Private Tax Index (sector-aggregated PTB)

- ECR Efficiency Comparison Ratio (model-to-model multiplier)

- LTE Index Life Time Efficiency Index

- TEI Time Extraction Index

- T Time — work hours required to fund the service

- SD Services Delivered

- PLT / CLT Permanent / Community Land Trust